Guest post. Originally posted on The Next Web.

----

I realized the other day that we’ve grown from $0 to $1 million with two separate products (HelloSign and HelloFax). This happened a long time ago, but I was recently reflecting on the lessons.

I found a lot of growth truisms to be false. We’ve learned a lot. Some lessons were painfully won, which is why I may sound strongly opinionated about them. They also may be slanted towards B2B products, but I wouldn’t discount them if you’re not in that space.

Here are our lessons:

1. Charge for your product as soon as possible. Really.

Every founder I talk to has a good reason for not charging for their product and it’s usually a bad reason. I remember office hours with Paul Graham. We explained that we were focusing on product now, but would focus on revenue later. He was confused, that somehow we saw a tradeoff between focusing on product and focusing on growth. Building product should equal growing revenue. People show they value your product by paying for it.

2. Revenue tells you what features to focus on

Charging is a powerful indicator that you’re building something people want. If you’re not charging, you’re likely spending money (development time = money) building features your users don’t really want. People who pay you have opinions about what to build next. Making them happy will lead to more people like them paying you (with this caveat: Don’t build a Galapagos product)

3. Focus on the right customer

YC and Paul Buchheit often say find one user and make her happy. I’d amend that. Find one user in a big market that has the highest LTV, lowest churn, and focus on making her happy. Otherwise, you may be boiling the ocean.

4. ‘You have a distribution problem, not a product problem.’

After one board meeting, our investor said, ‘you have a distribution problem, not a product problem.’ It’s a lot easier to change your message and re-focus on a different target market than completely changing your product. Do that before pivoting or rebuilding your product.

5. “Cheaper and better” doesn’t necessarily lead to higher conversions

Cheaper and better is another truism I found mostly false. Customers often doubt a product is better, because it’s cheaper. Strange, I know. I remember one of the Wufoo founders explaining the notion of being more expensive and better. Plus, if you charge more, you can invest more in product and truly make it better.

In fact, I met one CEO who deliberately priced his product higher than his competitors, just to get them to ask, ‘why’. Then, he’d pitch why his service was better than the competitors. When we split tested our pricing, just being cheaper didn’t lead to higher conversions.

Maybe there’s some scenarios where cheaper and better could make sense, but I think this truism needs to be questioned and perhaps the default truism should be reversed: be more expensive and better.

6. Being too cheap or free can lead to less growth

It turns out that distributing to businesses takes money and effort. They don’t just show up. Since we had cheaper plans, we couldn’t afford to reach out to more customers. But, with more expensive plans and a higher LTV, we can spend significantly more to acquire customers.

Being ‘cheaper’ and ‘better’ really just makes it so you can access less people.

7. There isn’t a strong correlation between beautiful design and success (in the early days)

Let me preface this by saying, we love design. I’m a huge fan of design and we’re making a big investment now. I think it’ll help us get to the next level.

I remember meeting with Garry Tan, who is an incredible designer. He mentioned that he hasn’t seen a strong correlation between good design and success of startup companies. So, if you have to choose, pick great user experience, then add great design later.

Conversely, focusing on pixel perfection in the early days may even prevent you from getting the revenue you need.

8. Free plans often make business leads feel uncomfortable

A huge customer wanted to use us for thousands of seats. Instead of being excited by our free plans, they just got confused. We lost them. That was painful. Not paying means that you may not be around forever. Paying money for software signals that they can depend on you for this really important function in the future.

Startups underprice all the time. As a business, we signed up for a $15 / month tool. I would have paid $100 / month for the value it provided. I had an unusual moment, where instead of getting excited about how inexpensive it was, I got nervous about using a key piece of software for only 15 dollars per month.

9. Don’t listen (too much) to your users on pricing

Innovate on your product, not the pricing. We’ve tried all types of innovative pricing models, often driven by our user-base, which have resulted in a lot of custom development. Ironically, when we switched back to industry standard pricing, the plans performed significantly better.

10. $5 / month is too cheap

If you’re a business tool and charge $5 / month, you’re likely leaving a lot of money on the table. Justin Kan said that we were running a charity. He was right. We doubled our prices. See #9.

11. Split test pricing early and often

Two years after launching, we doubled our pricing without an impact on churn or conversion. Since we grandfathered all of those users, we have two years of paid plans that could have been paying us $10 / month versus $5 / month. If we had done this split test earlier, we would have effectively doubled our revenue.

To visualize the impact, imagine a company with 1,000 paid customers:

$5 / month = $5,000 MRR (monthly recurring revenue) and $60,000 in ARR (annual recurring revenue).

$10 / month = $10,000 MRR and $120,000 in ARR

That could be the difference between succeeding and failing as a company.

12. Try to be profitable, at least once

I often meet with founders who tell me that they’re working on free user growth. I’m going to say something controversial: with rare, rare exceptions, you should never just focus on free user growth at the expense of revenue unless you’ve previously been profitable or run a profitable company. I don’t think most new founders know how to make the optimal tradeoff between free and paid user growth.

I remember having office hours with Emmett Shear. I explained that we were focusing on user growth, at the expense of revenue growth. He asked if our company would be harmed by focusing on revenue for six months? From that moment on, we started one of the biggest revenue ramps we’ve ever had.

If you’re not convinced, you should read this amazing article by Mark Suster on revenue.

13. Your number of paid plans will gets messy, and that’s ok

I remember being reluctant to split test pricing plans, since it’d produce more paid plans to support. Then, we did it. Sure, it’s extra work to support them, but it’s well worth it to double your revenue.

14. Prosumers have higher churn

Yep, and the difference is dramatic.

The only way for prosumers to potentially work is if they have an extremely high frequency activity with your product – something they do so often, they see so much value, that they pay, like Evernote or Dropbox. Plus, there really needs to be a massive number of people that could use your software. However, that type of mass market prosumer software is few and far between.

15. The Dropbox referral page is amazing for Dropbox, but does it work for you?

Dropbox has an amazing referral page, where users can perform actions, like inviting friends, in exchange for free storage. It’s been a big source of growth for them and I’ve seen a lot of other companies try it. Of all of the companies I’ve met, I’ve never heard of it becoming a meaningful source of growth.

16. “I don’t use it enough” or “It’s too expensive” means they’re the wrong customer

Some founders react to this feedback by lowering their prices. That’s typically the wrong thing to do. If someone doesn’t use a product often, she’ll always complain about the price, because she won’t see the value in it.

That just means she’s the wrong customer. Instead, find people that use your software often or fix a bigger pain point. See #3.

17. Startups will probably be your first users and complain the most about pricing

Be careful about listening to them, otherwise you may start developing your product or pricing in unnatural ways, which have nothing to do with the real market. We’ve done that and regretted it.

18. Free users make the most noise, but pay the least

We certainly give the best support possible to our free users, but we take their feature requests with a grain of salt. If you listen too closely, you may take your product in suboptimal directions. Build features for the people that pay you.

19. Month on Month (MoM) growth is key

I can’t emphasize this enough. This is what separates lifestyle businesses and startups (PG: Startups = Growth). Build 20 percent+ MoM growth and you could be the next Dropbox.

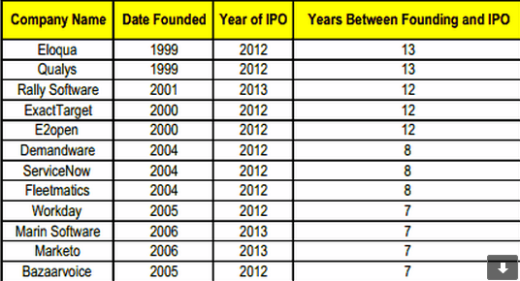

20. It takes years to stack revenue

Even with high growth, revenue takes time to grow. Average IPO is 7-13 years. It takes time to stack paid plans every year. But, if you have high MoM growth and minimize churn over time, revenue adds up.

21. Eventually, you need marketing and sales

The danger of the product CEO is that when you love product, every solution is a product solution. Dropbox is one of the very, very, very few companies where this worked out – a group of MIT grads sitting in a room, building great product and viral loops.

However, in the more common world, word of mouth only gets you so far. Marketing, Sales and BD are what make companies grow. Great product just makes it easier.

I met with someone who buys startup companies at low prices that are running out of money. He then implements very standard tactics to make them grow revenue. None of these things are rocket science. These companies then turn into revenue machines. His impact is immediate and mind-blowing.

It’s unfortunate that the founders missed the chance to drive it themselves. Founders will often wait for a natural lift in growth and will keep changing their product until it gets there – even when changing the product no longer make sense.

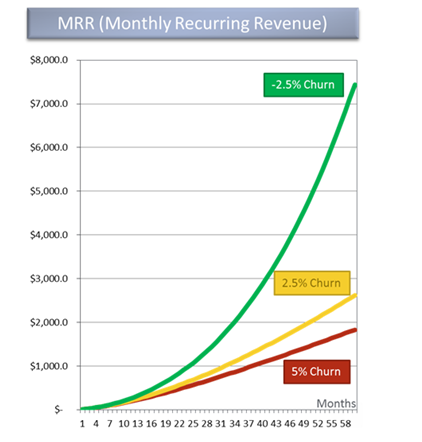

22. Small variances in churn can have a massive impact on revenue growth over time

This is the best graph on churn I’ve seen. Small differences in churn has an exponential impact on your MRR over time. See below.

Unless you get control of churn, your growth will eventually stop, since churn will cancel out any new upgrades. It’ll become more and more difficult to replace churned users over time.

23. Annual plans are amazing. Implement them ASAP.

You offer your users a discount for the year and in exchange, you get approximately 10 months worth of revenue right away (depending on how you discount), rather than one month of revenue each month. That can easily make the difference between being cash flow positive and burning money. It can also reduce churn and many of your customers prefer them. Win, win. Plus, when those renewals hit after one year, your revenue takes a big jump. If I were you, I’d implement annual plans ASAP.

24. Engagement is a leading indicator for revenue

Engagement is flat, but revenue growth steady? That probably won’t last. There’s only so much you can do before paid upgrades decrease.

25. Focus on a limited number of metrics

As much as I love metrics, focus your attention on just a few. I’d pick one revenue growth metric, one churn metric and one engagement metric to start. Then, grow your metrics dashboard over time. When you do, implement this one.

We started out with a metrics setup that was really complex and all we got was a lot of wasted time and an important lesson.

26. For fundraising, revenue growth slides are more powerful than free user growth slides

This may be controversial, but I completely pulled our free user growth slide from our deck and stuck it in the addendum. Investors were way more receptive to our pitch. Free user growth is just a proxy for future revenue. So, if you have revenue, just show that instead.

27. Hone in on ‘deal breaker features’, not feature requests

There’s something powerful about someone saying they won’t sign up unless you have X feature or canceling because you don’t do Y. Anyone can have a feature request. Few people will vote with their feet.

Building those deal breaker features will produce more revenue.

28. Always know your runway

I still meet with founders getting blindsided when they realize they’re almost out of money (Don’t be the startup that accidentally runs out of money). Knowing your runway allows you to make smart decisions about revenue and fundraising, early. Just knowing when you’ll run out of money is healthy, since it guides your daily decisions on revenue.

29. Your free users are for marketing

I remember an experienced CEO explaining to me that free users are just one part of the funnel. She thinks of supporting those free users as part of the marketing budget. They spread the word. They become engaged and upgrade later. But, think of them in that context.

30. Growth is not magic and it isn’t a black box

It’s something companies do or don’t. They do it well or don’t. There are tried and true tactics out there.

I see a lot of almost desperate innovating when it comes to growth. Sure, keep looking for the hacks and viral loops. Maybe you’ll come up with your own equivalent of the Dropbox referral page. But, while you’re doing that, there are a ton of sources of growth that are tried and true over the years. You just have to build those channels: BD, PPC, SEO, channel partners, PR, content, API evangelism, viral and more.

31. Business development can do wonders for revenue, if done right

We learned a lot of business development (BD) lessons, some of them were painful. There are a lot of pitfalls when it comes to doing BD when you’re a startup. But, it can (and has) become a huge source of growth. Here are some of the lessons I talked about at a talk at 500startups.

32. Doing paid advertising can improve your entire funnel

There’s nothing like paying money for advertising to make your entire funnel more disciplined. We changed our onboarding, emails, and pricing, all to make our campaigns profitable. The paid ads were only a minuscule part of our growth. But, the rest of the product hugely benefited from those optimizations.

33. Product market fit

Product market fit = entire team (product, bd, marketing, engineer) focused on one market & killing it, in a predictable way. That’s the end goal.

34. Do post mortems on every release

It’s humbling when you make a big investment on a feature, only to have no one use it or pay for it. Do this once and it completely changes how you think of every feature you build.

35. Customer development != growth

Do customer development to focus on the right users. But, don’t get stuck in customer development / research cycles. Customer development is important, but should have a completely different place in your mind as growth. I see lots of companies stuck in customer development cycles, but as a consequence, these companies might never focus on distribution.

36. All word of mouth growth makes some investors nervous

Word of mouth is nice, but it’s not predictable. You need predictable growth.

37. If you build it, they won’t just come

I’ve seen companies go under, waiting for the users to come. They never came.

38. It’s less stressful when you generate revenue

Startups can be stressful. A lot of people have written about founder depression – it’s a real thing. Sam talks about how founders have a lot of weight on their shoulders. Having revenue can significantly ease that weight.

39. Put together a hypothetical pricing page with a spreadsheet and how it’d look when you fill it out with features

That spreadsheet will help guide product development, since everything is connected to revenue. Put higher value features on the higher plans.

40. Customers don’t price shop as much as you think

Our price, in relation to our competitors, doesn’t come up often. Sometimes we’re more expensive, yet we might still win the deal. So, don’t become too obsessed with your competitor’s prices. Just optimize for your users.

41. If you’re only winning on price, rethink the value you add

Unless you’re Amazon, a price war can be brutal. Instead of being cheaper, think about how to differentiate.

42. Consumers and businesses behave differently when it comes to money

As a company, we pay a huge amount of money for software and don’t flinch, but in my personal life, I’m still on a free Spotify account. Many founders don’t have real work experience before starting a company, myself included. Without being in a work environment, it’s hard for a founder can imagine how much companies pay for software, which leads to underpricing their product.

43. If you’re a SaaS product, read this post over and over again

This is easily the best SaaS analytics post I’ve read.

Revenue isn’t a bad thing. Want to know what we do with revenue? We support a team of terrific people that help us build and support this product. Every day we make the product better, because we have revenue. The more revenue you have, the better you can make your product for your customers.

For some reason, the mental default for founders is that their product should be free – and charging needs to be justified. The inverse should be true – the mental default should be that your product should be paid and being free should be justified.

In fact, most pricing truisms should be reversed. Statements like “cheaper and better” should need to be justified, instead of spoken and accepted as truth.

Today is a good day to grow revenue! No reason to wait. I find it weird that I meet with founders and have to convince them that growing revenue is important. Then, runway decreases, they can’t raise, the game is over and everyone acts surprised. (Don’t be the startup that accidentally runs out of money)

In fact, if you this figured out, you may get to the mythical, ‘infinite runway’. Then, if you want, you can turn on the spigot and operate at a loss in exchange for revenue growth. That’s the moment increasing your burn rate for growth makes sense, but rarely before.

{kind=link}

{kind=link}